There are two primary ways to increase the return on an investment (ROI)—decreasing costs or increasing value.

A college degree is a significant investment, often funded through a variety of funding sources. Whether you're borrowing, using savings, or have scholarships, there are ways to increase the value of a degree, including short- and long-term strategies.

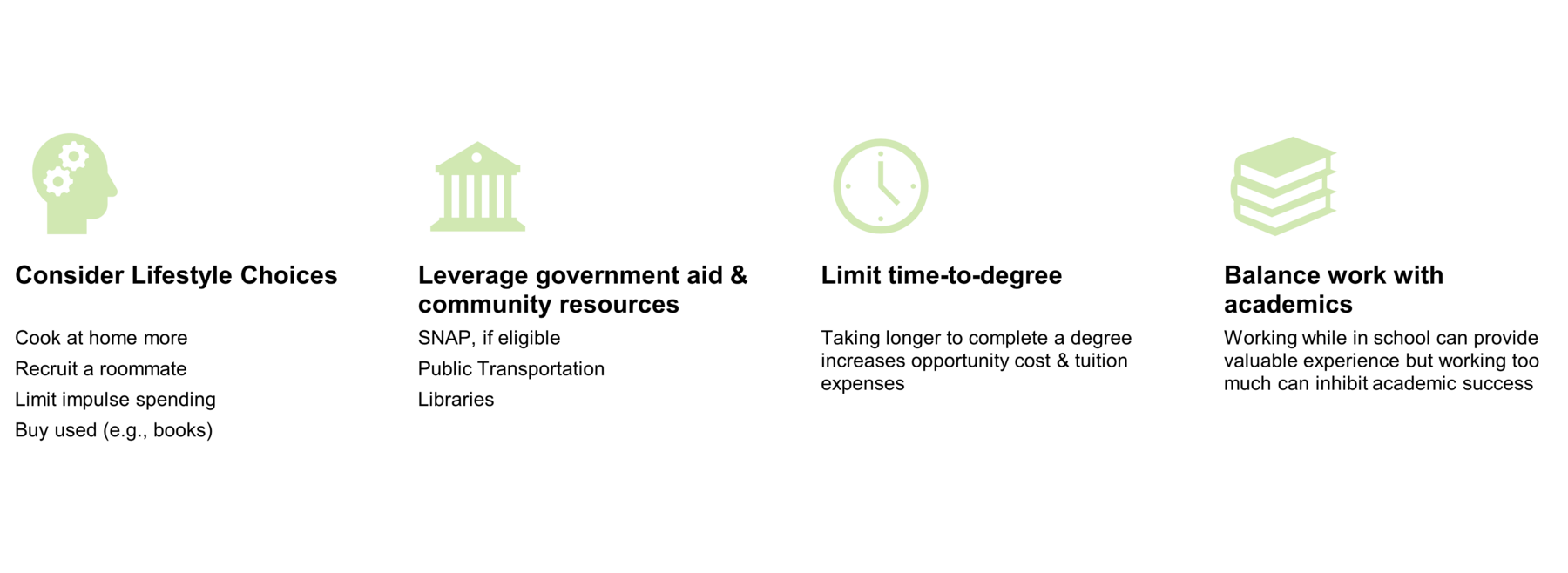

Ways to Save

There are several ways you can save money while making progress toward your degree.

Consider Lifestyle Choices

You may want to consider lifestyle choices such as:

- Cooking at home more often

- Recruiting a roommate to share housing costs

- Looking for ways to limit impulse spending

- Buying used items rather than new whenever possible (such as textbooks)

Leverage Government Aid and Community Resources

Besides financial aid from the Free Application for Federal Student Aid (FAFSA), you can also explore government aid and community resources to help save money. Illinois residents should also investigate state-specific aid opportunities through the Retention of Illinois Students and Equity (RISE) Act, which provides additional support for eligible students.

If you work while in school, you may be eligible for the Supplemental Nutrition Assistance Program (SNAP) to cover some of the costs of food.

Most universities in the University of Illinois System offer either discounted public transportation passes or allow you to use your iCard to access public transit for free.

After analyzing all your options for paying college costs, you may need to revise your budget. Since living expenses can make a big difference in the cost of your education, looking for ways to cut costs through your lifestyle choices is an immediate strategy for lowering your overall costs. For additional guidance on budgeting and financial planning, visit our page on budgeting.

Limit Time to Degree

You also want to limit the time it takes you to complete your degree. If you are working while going to school, look for a way to balance work and school responsibly. Working while in school can provide valuable experience, but working too much can lower grades and inhibit your ability to complete your degree.

The chart above illustrates the financial impact of extending time to degree using data related to University of Illinois Springfield (UIS) graduates.

Completing a bachelor's degree in 4 years costs approximately $47,228 in average net costs (tuition, fees, room, board, and other expenses after financial aid). However, taking 5 years increases the total cost to $106,467—that's $59,035 in additional net costs plus $47,432 in potential lost income from delaying entry to the workforce by one year. If it takes 6 years to complete the degree, the total rises to $165,706, which includes $70,842 in net costs and $94,864 in lost earning potential.

These opportunity costs represent money that graduates could have been earning if they had entered the workforce on time. The average starting salary for UIS graduates means that each additional year delays not just one year of income, but also delays career advancement, retirement savings, and wealth building. While completing your degree is always better than not finishing, this comparison demonstrates why it's financially important to stay on track and graduate within the standard timeframe whenever possible.

Understand Compound Interest

Above is a chart of an amortization schedule for a student loan. Consider the following example where you start repayment immediately after disbursement rather than at the end of a 6-month grace period after leaving school:

Loan Details:

- Principal loan balance (amount borrowed): $35,000

- Annual interest rate: 6.53%*

- Loan period (term): 10 years or 120 monthly payments

- Payments start: October 15, 2026

- Monthly payment: $397.95

- Total interest paid: $12,754.28

- Total cost of loan: $47,754.28

*Note. 6.53% was the rate for loans disbursed between July 1, 2024 and June 30, 2025 (U.S. Department of Education, 2024).

What we want to highlight is the grey loan balance line. With the way compound interest works, you pay more interest at the beginning of your loan, so the principal balance—that $35,000 that was initially borrowed is slow to decrease. You don't pay off half of the initially borrowed amount until about 6 years into repayment.

This works similarly for other types of loans, like mortgages and vehicle loans.

Part of the reason that you pay more interest at the beginning of your term is because of compound interest. This is when interest is added to the principal balance of the loan and the next month the interest is calculated based on this higher total balance.

Lowering Compound Interest Costs

For unsubsidized student loans, interest starts accruing from the day you take out the loan—even while you're still enrolled. If you don't pay this interest as it accumulates, it gets capitalized (added to your principal balance) when you enter repayment. This means you'll pay interest on a larger amount.

Paying interest as it accrues, even in small amounts, can reduce your total loan cost.

This is generally true for undergraduate student debt, but it can be more complicated for graduate and professional degree seekers with higher costs and more limited opportunities to generate income while in school.

It may be better to reduce your overall costs and cancel part of the loan depending on your situation (such as if you're a medical student who cannot work while you're in school and the payments on interest alone would be significant).

Example 1: $20,000 Principal + 6.5% Interest

If you took out a $20,000 unsubsidized student loan at 6.5% interest as a freshman, paying the interest as it accrues—before it is capitalized (or added to the principal balance of the loan)—would be about $108 per month until graduation.

This example assumes you take out $20,000 in your first semester and don't add any loans, just to simplify the illustration of how compound interest impacts the total amount you pay.

Amount Borrowed and Interest Rate

- Principal borrowed: $20,000

- Interest rate: 6.5%

- Standard repayment upon graduation: 10 years or 120 months

Details if Paying Interest While in School

- Interest paid per month if paying while in school: $108.33 per month

- Total paid during 4 years in school: $5,200

- Balance entering repayment if interest paid in school: $20,000

- Monthly repayment amount upon graduation if interest paid in school: $227.10 per month

Details if Not Paying Interest While in School

- Balance upon entering repayment if not paying while in school: $25,920.41

- Monthly repayment amount upon graduation if not paying while in school: $294.32 per month

Comparing Total Costs

- Total amount paid if interest paid while in school: $32,451.51

- Total amount paid if interest not paid while in school: $35,318.52

Potential savings: Paying the interest as it accrues could save you $2,867.01 over the life of the loan if you repay it within 10 years after graduation. That savings could be put toward building wealth or accomplishing other goals you have.

Example 2: $100,000 Principal + 8% Interest

However, let's say you're in a higher-cost, more intensive degree program, like dentistry or medicine, where it could be extremely difficult to earn extra income to make interest-only payments while in school. It is less costly to try to reduce the amount you borrow initially, if you're able, than to attempt to make interest-only payments while in school.

The interest rate for federal student loans for both undergraduate and graduate students varies every year (U.S. Department of Education, 2024). We used 6.5% and 8% in these examples to approximate current rates while simplifying the illustrations around compound interest.

In this scenario, if you chose to pay interest while you're in school on a $100,000 loan at 8% interest, your interest-only payment would be approximately $667 per month.

However, reducing initial borrowing by $8,300 (to $91,700) and not paying interest as it accrues saves approximately $9,000 total over the life of your loan compared to making interest payments during school, and saves $13,100 compared to not paying interest and allowing it to capitalize—all using the standard 10-year repayment plan. This demonstrates that for high-cost degree programs, reducing the amount borrowed initially can be more beneficial than attempting to make interest payments during school.

Leveraging Opportunities at Your University

Increasing the return on your degree isn't just about reducing costs, though. It's also about leveraging the opportunities you have at your university. Each of the universities in the University of Illinois System offers unique experiences and services to students.

Determining Value of Experiences

The value that an individual places on experience varies from person to person. It could be measured objectively or subjectively. An example of an objective measurement might be the cost of a particular class, while an example of a subjective measurement might be intangible, like the friendships you gain from volunteering with a student organization.

You may value the career skills and knowledge your academic studies are preparing you for, but there are other opportunities for growth and developing healthy habits through student support services, student organizations and clubs, and even the communities surrounding our universities. Take time to reflect on which opportunities will give you the type of value you want out of your college experience.

Time is finite, so prioritizing what you value most right now and what you may not be able to have access to later in your life can help you identify what you want to focus your efforts on during your time in school. You don't have to collect all of the experiences right now. You can be strategic so you don't burn yourself out.

Career Services

Career services can give you the knowledge and skills to help you during the job search and throughout your career. Understanding post-graduation outcomes can also help you make informed decisions about your degree investment. The U.S. Census Bureau provides Post-Secondary Employment Outcomes (PSEO) data showing employment rates and earnings for graduates from specific institutions and programs.

Check out the career services office at your university:

Networking

The strength of your network is difficult to measure. However, it is clear that networks are important for both social support and mobility in our careers. You can use an objective measure of connections, like those on LinkedIn, but it doesn't necessarily identify how strong your connections to each of those people are or how it may help you navigate transitions throughout your career.

Leverage opportunities to build your network while in school and learn how to maintain and build those relationships throughout your life.

Summary: Strategic Approaches to Maximize Your Degree's ROI

Increasing the return on investment for your college degree requires a multifaceted approach that balances cost reduction with value maximization. The strategies outlined in this article fall into three primary categories:

Immediate cost-saving strategies include making smart lifestyle choices (cooking at home, finding roommates, limiting impulse spending), accessing available government benefits like SNAP and free or low cost public transportation, and most importantly, completing your degree on time. Extending your time-to-degree from 4 to 5 or 6 years significantly increases both direct costs and opportunity costs from delayed employment.

Financial literacy strategies focus on understanding and managing student loan debt effectively. By understanding how compound interest works, you can make informed decisions about whether to pay interest as it accrues during school or to focus on reducing your initial borrowing. For undergraduate students with smaller loan amounts, paying interest during school can result in significant savings. For graduate and professional students facing higher loan amounts and limited earning capacity during school, reducing initial borrowing is often the more effective strategy.

Value-building strategies recognize that ROI isn't solely about minimizing costs—it's equally about maximizing the value you receive. This includes taking full advantage of career services, building a professional network, participating in student organizations, and strategically selecting experiences that align with your personal and professional goals. These investments of time and energy during college can yield returns throughout your career.

The most effective approach combines all three strategies: be intentional about managing costs, make informed decisions about financing your education, and actively pursue opportunities that will provide lasting value beyond graduation. By taking a comprehensive, strategic approach to your college investment, you can significantly improve your degree's return while building the foundation for long-term success.

References

Illinois Department of Human Services. (n.d.). Supplemental Nutrition Assistance Program (SNAP). https://www.dhs.state.il.us/page.aspx?item=30357

Illinois Student Assistance Commission. (n.d.). Retention of Illinois Students and Equity (RISE) Act. https://www.isac.org/students/before-college/financial-aid-planning/retention-of-illinois-rise-act/

U.S. Census Bureau. (n.d.). Post-Secondary Employment Outcomes (PSEO). https://lehd.ces.census.gov/applications/pseo

U.S. Department of Education, Federal Student Aid. (n.d.). Federal student aid. https://studentaid.gov/

U.S. Department of Education, Federal Student Aid. (2024). Interest rates and fees for federal student loans. https://studentaid.gov/understand-aid/types/loans/interest-rates

University of Illinois System. (n.d.). Student money management. https://www.studentmoney.uillinois.edu/